Medical Debt

Have you ever received a medical bill that you couldn’t afford to pay? Or maybe you avoid going to the doctor, even when you really need to, because you fear the costs. Does the idea of opening medical bills stress you out or cause a full-blown anxiety attack? Or worse, you feel depressed and hopeless, fearing the medical debt will never be paid off. If medical debt is stealing your peace of mind, you’re not alone.

Medical Debt in the U.S.

Medical debt, or personal debt incurred from unpaid medical bills, is a leading cause of bankruptcy in the United States. Over 40% of Americans — over 100 million people — carry some form of medical debt, including money owed to providers or relatives, or on credit cards and other loans. About one-fifth of people with medical debt don’t think they can ever completely pay it off.

Check out our blog article, Medical Debt: A Threat to Your Finances to learn more.

What about Health Insurance?

Health insurance often falls short of delivering adequate financial protection. According to KFF polling data, 42% of U.S. adults with health insurance report difficulty affording medical costs. Among this group, 36% report skipping or postponing care, and 37% report not getting the health care they need due to cost. Due to high deductibles and cost-sharing, coupled with increasingly high healthcare prices, you can be left underinsured and exposed to unexpected medical expenses.

Medical Debt and Your Credit

Medical debt can ruin your credit score! In most states, medical debt over $500 can be reported to credit reporting agencies and sold to aggressive third-party debt collection agencies. Hospitals or debt collectors can usually charge interest on medical debt as well, compounding the debt.

Bad credit can prevent you from accessing credit and financial opportunities, such as getting a better interest rate on credit cards or loans — if you can even get one. Medical debt can also prevent you from getting a job, buying a car, or leasing or buying a home. In the worst cases, it could eat up your savings or retirement funds and lead to bankruptcy.

Check out our blog article, 8 Steps to Keep Medical Debt Off Your Credit Report.

Medical Debt and the Legal System

After ruining your financial life, the negative consequences of medical debt don’t end there.

In most states, hospitals, providers, and debt buyers can sue patients to collect on unpaid medical bills. A KFF Health News investigation found hundreds of U.S. hospitals weaponizing the courts against patients with unpaid medical bills. Included in this list were academic hospitals and nonprofit facilities that receive tax benefits for providing financial assistance programs to qualified patients.

These lawsuits often result in wage garnishments, money taken out of bank accounts, liens, and foreclosures — even for patients who should have qualified for charity care! In some locations, doctors’ offices, dentists, and other providers are starting to sue patients for unpaid bills more than hospitals are. Businesses note that they need to get paid, but critics of medical lawsuits say they are often filed over very small amounts that would not make much difference to big companies.

Medical Debt Rights

The main federal laws that provide some legal protections against medical debt are the Fair Credit Reporting Act (FCRA), Fair Debt Collection Practices Act (FDCPA), and the No Surprises Act. The FCRA regulates how debt can be reported on your credit report, and the FDCPA regulates debt collection practices.

The federal No Surprises Act protects individuals with most private insurance plans against some unexpected bills, particularly for emergency care and certain out-of-network charges. It also protects the uninsured or those paying cash. If you got an estimate in advance and your bill is more than $400 higher, you can dispute the charges within 120 calendar days of receiving the initial bill.

Relatively few states regulate billing and collections practices or limit the legal remedies available to creditors.

Follow Decoding Health Care for more on federal and state debt collection laws and regulations in our coming article, Medical Debt Rights and Protections.

Medical Debt Can Kill You!

Denial of Non-Emergency Healthcare Services

According to KFF polling, 1 in 7 people with medical debt said they’ve been denied access to a hospital, doctor, or other provider because of unpaid bills. Although federal law says you can’t be turned away in an emergency when you seek medical care at the hospital ER, the rules for non-emergency healthcare are very different.

The Emergency Medical Treatment and Labor Act (EMTALA) ensures public access to hospital emergency medical care — regardless of your ability to pay or insurance status. It requires hospitals that accept Medicare and provide emergency services to screen and “stabilize” you, not provide all your follow-up care, which costs more. And EMTALA doesn’t mean free emergency care — you will usually still be charged.

For scheduled, non-urgent healthcare services, providers can deny or restrict care. For a patient with outstanding medical debt, the facility may:

- Pause treatment until balances are addressed

- Require payment upfront (especially for expensive procedures)

- Refuse to schedule services if you have unpaid bills or you’re not making payments on past medical debt

- Require you to set up a payment plan

- Require partial or full payment before future care

- Pressure you to sign up for a high-interest medical credit card

Psychological and Health Effects of Medical Debt

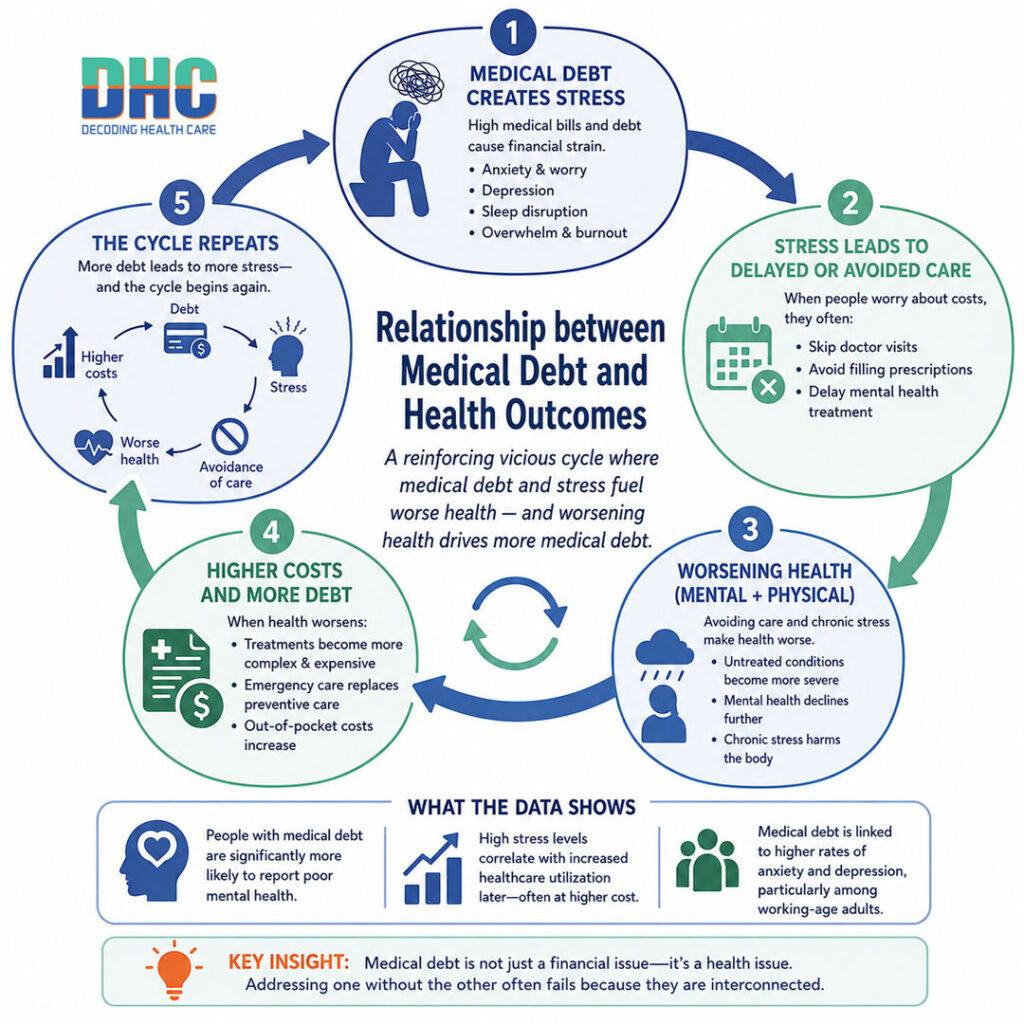

The stress associated with medical debt can be detrimental to your physical, mental, and emotional health. Individuals with medical debt commonly report depression and anxiety. This is sometimes worsened by malnutrition, resulting from cutting back on food and necessities. Nearly 40 percent of adults who have incurred medical debt say they’ve had to cut back on basic necessities like food, heat, or rent.

Fearing more debt, they often delay or skip seeking healthcare services. They frequently ration their prescriptions or don’t fill them at all. Nearly 1 in 3 people (31.8%) with chronic conditions reported their health has worsened because they could not afford medication. When medical debt becomes a barrier to healthcare, worsening health, more debt, and higher mortality rates follow. In this way, medical debt creates a self-reinforcing loop — driving stress, delaying or skipping care, worsening health (mental and physical), and increasing medical debt.

Financial Toxicity

The financial strain and the emotional stress that patients and their families face due to the high direct and indirect costs are referred to as financial toxicity. One study estimated that financial toxicity affects approximately 137 million adults (56%) when considering all its aspects in various diseases. More study participants reported the psychological burden (43%) over the financial cost burden (26%). This is why some people can’t even open their bills without triggering severe anxiety that prevents them from confronting the debt. Paradoxically, the very system that is supposed to heal you can kill you!

Decoding Health Care Can Help

If you’ve read this far, you know that medical debt is not only a financial issue, but a health issue. Of course, if you never go to the doctor, you’ll never have to worry about debt. However, that can lead to a dangerous cycle that ends up making you sicker—with more debt.

No one should have to suffer medical debt and financial toxicity just because they got sick or injured. Through educational content, Decoding Health Care aims to guide you on the path that leads to patient financial wellness. With or without insurance, you can navigate the healthcare system while minimizing its costs. Additionally, you can learn strategies to help you avoid, reduce, or even eliminate dangerous medical debt.

Check our blog article, How Can I Get Help with Medical Debt?

New tips, strategies, and tools for outsmarting the medical billing system and saving on healthcare expenses are continually being discovered. Laws governing medical debt, health care, and insurance also change. To keep up, we have a free monthly newsletter devoted to patient financial wellness, the DHC Insider. It’s written by human subject matter experts in the fields of health insurance policy and medical billing advocacy.

Let Decoding Health Care guide you through the healthcare system “obstacle course” without losing your finances, health, or mental well-being.

Key Points

- Over 40% of Americans carry some form of medical debt.

- Insured and higher-income individuals also carry medical debt due to high deductibles, cost-sharing, and high healthcare prices.

- Medical debt can ruin your credit score, limit your financial opportunities, eat up your savings, and potentially lead to bankruptcy.

- In most states, hospitals, doctors’ offices, dentists, other providers, and debt buyers can sue patients for unpaid bills.

- The Fair Credit Reporting Act (FCRA) regulates how debt can be reported on your credit report.

- The Fair Debt Collection Practices Act (FDCPA) regulates debt collection and credit reporting practices.

- The No Surprises Act protects most insured individuals against some unexpected, surprise bills. It gives those not using insurance the right to receive an estimate in advance and dispute the bill if it’s more than $400.

- Relatively few states regulate billing and collections practices or limit the legal remedies available to creditors.

- The Emergency Medical Treatment and Labor Act (EMTALA) ensures public access to screening and stabilization emergency medical services, regardless of current medical debt or insurance status.

- For scheduled healthcare services, providers can deny or restrict care if you have outstanding medical debt.

- Medical debt is a barrier to healthcare, creating a self-reinforcing loop — driving stress, delaying or skipping care, worsening health (mental and physical), and increasing medical debt.

- Medical leads to higher mortality rates — it can kill you!

- With Decoding Health Care as your guide, you can learn strategies to help you avoid, reduce, or even eliminate dangerous medical debt.

Article by Julie Gunstanson, Certified Medical Billing Advocate, and Lauren R. Jahnke, MPAff, Author of Decoding Health Insurance and the Alternatives: Options, Issues, and Tips for Saving Money.

Disclosures: This article provides general information about medical debt. For guidance specific to your situation, consult financial counselors, billing advocates, or legal assistance in your area. Decoding Health Care provides independent and educational information and does not endorse any specific insurance plans or other health coverage products. AI tools were used to assist with researching this article; however, human subject-matter experts always extensively revise, fact-check, edit, and approve our content.

Do You Have a Medical Bill You Can’t Afford or Medical Debt in Collections?

Before you pay that big medical bill, read this!

Get our Free Medical Debt Quick Start Guide.

By submitting this form, you agree to receive educational emails from Decoding Health Care. You will also receive our free monthly DHC Insider, an educational newsletter focused on protecting your finances from high healthcare costs and medical debt—with or without insurance. You may unsubscribe at any time.