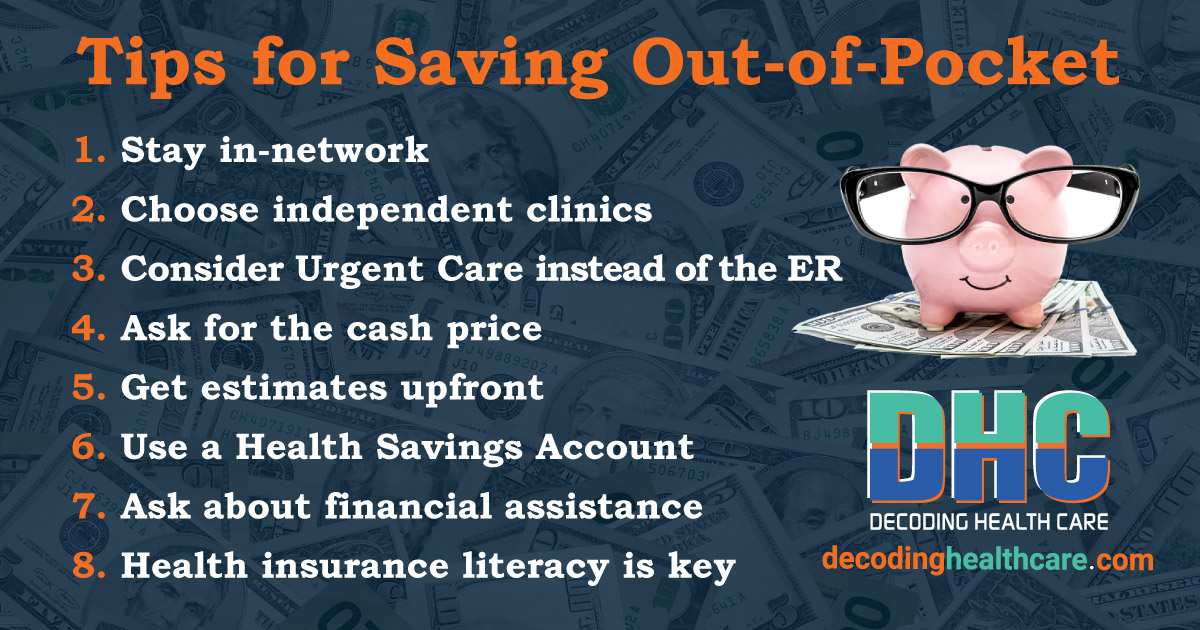

Top 8 Tips for Spending Less Out-of-Pocket for Health Care

We’ve all been there: opening a medical bill and feeling that immediate knot in your stomach when you see the cost. Even with “good” insurance, health care can feel like a maze of deductibles, co-pays, and unexpected charges. It often feels like the costs are completely out of our control.

The good news is you actually have more power than you think. By making a few small shifts in where you get care and how you pay for it, you can keep more of your hard-earned money in your pocket. Here are 8 practical tips to help you take charge and spend less out-of-pocket for health care.

1. Stay in-network when using insurance

When using insurance, you’ll spend less out-of-pocket by staying in-network whenever possible. Insurance companies negotiate lower rates with certain doctors and healthcare facilities (their “network”), and these networks can change. Although the No Surprises Act helps prevent some unexpected out-of-network charges, it’s always best to confirm your providers and facilities are in your network before scheduling planned care. This also applies to labs, anesthesiologists, and radiologists — common sources of surprise bills. You can find your network listed on your health plan’s website and search for providers or facilities (it may be called “provider directory”).

2. Choose independent clinics over hospital-owned facilities

Where you go for a medical test or a minor surgery can change the price by hundreds or even thousands of dollars. Many hospitals own smaller clinics or imaging centers, and because they are part of a hospital system, they are allowed to add an extra “facility fee” or administrative fee to your bill. This fee covers the hospital’s overhead, but it doesn’t change the quality of the care you receive.

To save money, ask your doctor if your blood work, test, X-ray, or procedure can be done at an independent facility. These are often called “standalone” imaging centers or “ambulatory surgery centers.” They usually provide the exact same services as a hospital, but without the extra layers of fees.

3. Use Urgent Care instead of the ER

Emergency rooms (also called emergency departments or EDs) are the most expensive place for care. ERs are designed for serious, life-threatening, or potentially disabling conditions. Yet many people use them for less serious conditions that could be treated at Urgent Care—or even primary care.

Urgent Care is often much less expensive than the ER and treats minor illnesses and injuries. It’s usually appropriate for conditions such as:

- Minor fractures or sprains

- Ear infections

- Flu or COVID symptoms

- Minor cuts needing stitches

- Mild asthma attacks

- Urinary tract infections

4. Ask for the cash price

Sometimes, the self-pay or “cash price” for a service or medication is actually lower than what you would pay using your insurance. So, always ask. Just keep in mind that if you pay cash, that money out-of-pocket might not count toward your annual insurance deductible.

5. Get estimates before your appointment

For planned, non-emergency health services, you can shop before you buy and get estimates. Most major insurance companies provide personalized “Cost Estimator” or “Find Care & Costs” tools within their member portals or mobile apps. These tools allow you to estimate your out-of-pocket costs, track your deductible and out-of-pocket maximum, and more.

If you do not have insurance—or if you have insurance but plan to pay for a service yourself—federal law gives you the right to a “Good Faith Estimate.” This is a written document from your provider or facility that lists exactly how much they expect to charge you for the visit or procedure.

You should ask for this estimate at least three business days before your appointment. Be sure to ask for estimates from all providers and facilities involved—the surgeon, anesthesiologist, radiologist, etc. If you receive the final bill later and it is at least $400 higher than the estimate they gave you, you have a legal right to dispute the charges through a federal process. This protects you from sticker shock after the care has already been delivered.

You can also compare prices for non-emergency care or prescription drugs using online tools such as Healthcare Bluebook and GoodRx.

6. Use a Health Savings Account to pay with pre-tax dollars

If you have a high-deductible health plan, you likely have access to a Health Savings Account (HSA). Think of this as a personal savings account specifically for medical needs. The big advantage is that the money you put into this account is not taxed. This means that if you are in a 20% tax bracket, using an HSA is essentially like getting a 20% discount on every medical bill you pay.

Individuals (or their employers) can contribute up to a certain amount each year to the HSA. The money stays in your account forever until you spend it—it does not disappear at the end of the year. You can use it for doctor visits, dental work, eyeglasses, and even many over-the-counter (OTC) pharmacy items like Tylenol. You can find a list of eligible services in IRS Publication 502 and more details on eligible OTC medicines from GoodRx.

Learn more about Health Savings Accounts and how to maximize their benefits in our article, How to Maximize Your Health Savings Account (HSA) and What’s New in 2026.

7. Ask about financial assistance or “charity care”

Most people assume that “charity care” is only for those without a job or a home, but that isn’t the case. Most nonprofit hospitals are required by law to have financial assistance programs. These programs often help families who make a decent income but are overwhelmed by a large, unexpected medical bill.

If you receive a large hospital bill, do not ignore it. Call the hospital’s billing office and request or download from their website the hospital’s financial assistance program application. Don’t wait, since there is a time limit after receiving a bill. Depending on your income and family size, the hospital may be required to lower your bill or even cancel it entirely. This is a legal protection for patients that often goes unused simply because people don’t know to ask.

If you know ahead of time that you will need to get hospital care, it’s best to apply for the hospital’s financial assistance program ahead of time. Learn more about charity care and how to apply in our article, How Can I Get Help with Medical Debt?

8. Health insurance literacy is the key to lower out-of-pocket costs for health care

If you have health insurance, reducing out-of-pocket healthcare costs often comes down to understanding how health insurance rules work.

Health insurance literacy is the ability to seek, understand, select, and use health insurance services. It includes understanding:

- Your Explanation of Benefits (EOB) and medical bills

- Navigating claims and appeals

- Cost-sharing and estimating out-of-pocket costs using your insurance plan

- Patient rights and legal protections

- Your insurance policy details, provider network, coverage, and exclusions

We hope you can use one or more of these methods to lower your out-of-pocket healthcare costs this year. For more money-saving tips, check out our book Decoding Health Insurance and the Alternatives: Options, Issues, and Tips for Saving Money.

Decoding Health Care is dedicated to providing educational materials that promote health insurance literacy and patient financial wellness, and help patients navigate the system—with or without insurance. Sign up for our free DHC Insider—a newsletter devoted to protecting your finances from our healthcare system.

Do You Have a Medical Bill You Can’t Afford or Medical Debt in Collections?

Before you pay that big medical bill, read this!

Get our Free Medical Debt Quick Start Guide and learn the first steps to take before sending a dollar to a medical provider or collection agency.

By submitting this form, you agree to receive educational emails from Decoding Health Care. You will also receive our free guide and free monthly DHC Insider, an educational newsletter focused on protecting your finances from high healthcare costs and medical debt—with or without insurance. You may unsubscribe at any time. Read our Privacy Policy.